Ahead of the rollout of the Insurance Corp. of British Columbia’s (ICBC) new risk model in September, private insurers are insisting that more competition is needed in the automobile insurance market to drive premiums down to a level comparable with those paid in other provinces.

“We’re seeing study after study that shows that not only do British Columbians pay more [than residents of other provinces] but the ICBC monopoly is more expensive for them,” said Aaron Sutherland, vice-president for the Pacific region at the Insurance Bureau of Canada (IBC), the private insurers’ national industry association.

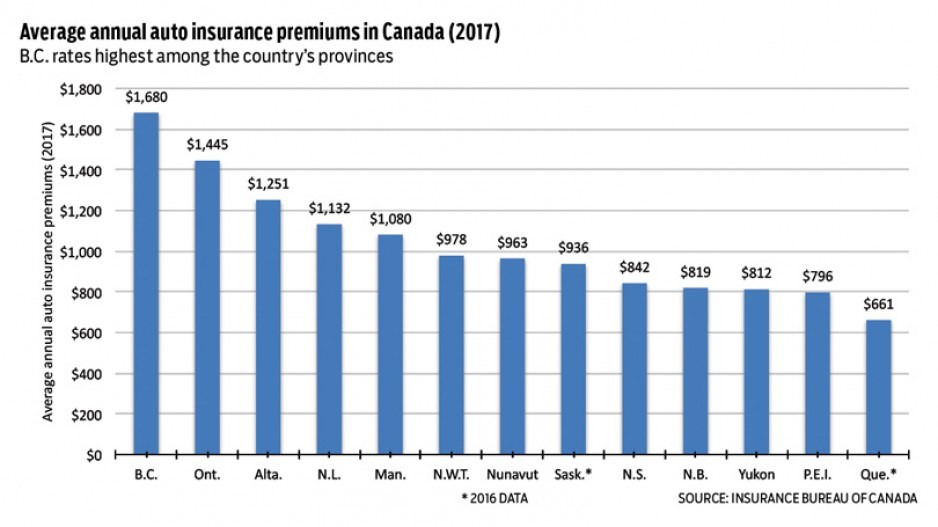

According to an IBC report, which used the latest available data from the General Insurance Statistical Agency, drivers in B.C. pay the highest auto insurance prices in the country, with an average annual premium of $1,680 — about 63 per cent higher than the national average.

These higher prices aren’t going unnoticed by B.C. residents. A recent national survey commissioned by Belairdirect found that 34 per cent of B.C. respondents said they are concerned with the price of their car insurance policy — more than in any other region in Canada. And 61 per cent of respondents said they strongly agree that they pay too much for their auto insurance, compared with 38 per cent for the rest of the country.

“We’re addressing the challenges within our current auto insurance system with the biggest reforms in B.C.’s history, which are already being instituted this year,” ICBC spokeswoman Jo-anna Linsangan told Business in Vancouver.

“And starting this September, auto insurance will be much more customized so that lower-risk drivers will pay less than higher-risk drivers. In fact, we anticipate more than 55 per cent of our full-coverage customers will be paying less than they do today.”

ICBC’s new risk model would shift the province’s basic auto insurance to a driver-based system, tying at-fault crash histories to drivers instead of vehicle owners. Premium reductions would be offered to drivers with less risky patterns of behaviour, as well as discounts for those driving vehicles with safety features like automatic braking systems.

However, IBC maintains that increased competition from private insurers would be required to turn the tide. A study commissioned by the organization and conducted by consulting firm MNP estimated that opening up the B.C. insurance market to increased competition would reduce premiums for around 60 per cent of drivers, with annual savings of up to $325.

Private insurers also say that even the limited amount of competition in the province’s auto insurance markets, in the optional insurance space where ICBC doesn’t hold a monopoly, isn’t allowing the industry to thrive and offer consumers better products.

“In theory, there’s competition here in British Columbia — the private sector is allowed to sell optional coverages,” said Colin Brown, president and CEO of North Vancouver-based insurance firm Stratford Underwriting and ICBC’s former chief underwriter.

“But the reality is that even after that’s been in place for well over 30 years, the optional coverage is only 10 per cent with the private sector and still 90 per cent with ICBC.”

Sutherland attributes this lack of competition in part to private insurers lacking access to ICBC’s data on claims and drivers, saying that without it insurers are “flying blind.”

“The biggest thing preventing true competition in optional auto insurance is the fact that ICBC will not share the data it holds for the marketplace,” he said.

However, whether it be through allowing private companies to compete with ICBC in the basic insurance market or by giving them access to data to improve their performance in the optional insurance space, not everyone agrees that increased competition is needed to improve auto insurance affordability in the province.

“We’re the professionals, we’re the ones who deal with clients, and our membership is kind of disappointed in the private insurance market,” said Chuck Byrne, executive director and COO of the Insurance Brokers Association of British Columbia, adding that competition can’t be expected to be a “magic wand” that solves every challenge the insurance industry faces.